Top Performing Investments That Most Financial Advisors Fail To Recommend

Financial investing expert, Stephen Leeb, explains that gold has been a top performing commodity investment and will continue to perform well in the future.

Vanguard recently ran a multi page ad in The New York Times that recommended investors own a diversified mix of equities and bonds. And that’s a totally unremarkable statement – the well-trodden path forever followed by investment houses and pension funds – typical allocation is 60% stocks, 40% bonds.

So why did I find this ad so striking? In particular, because of what it left out – which was any reference to commodities – and in particular to gold.

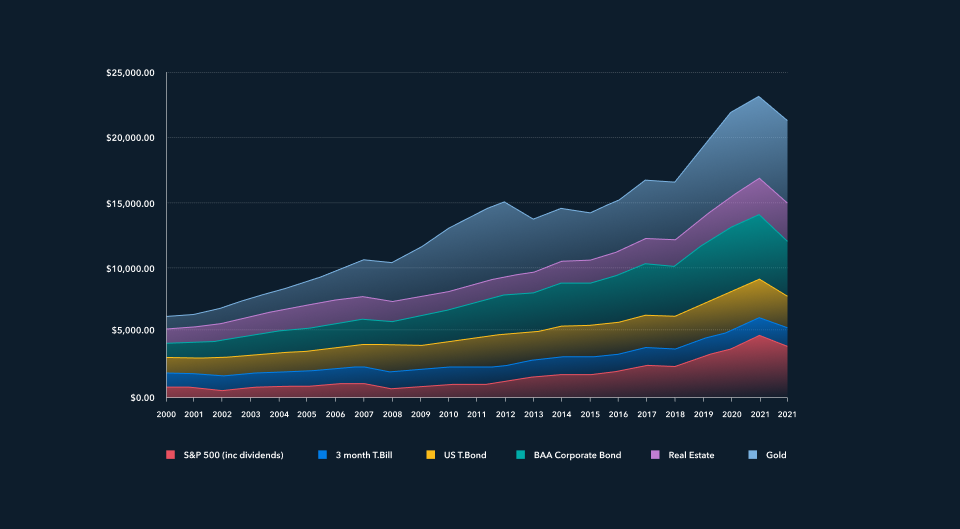

That’s astounding because Vanguard totally ignores that over the past 20 years, gold has been the top-performing asset class. It has outperformed stocks by 200 percentage points and bonds by more than 250 percentage points.

Between 2000 and 2022, a gold investment would have yielded you a 530.57% return. In 2020, as the pandemic gripped the world, its price surged by 24%.

Between 2000 and 2022, a gold investment would have yielded you a 530.57% return. In 2020, as the pandemic gripped the world, its price surged by 24%.

Gold has proven itself to be a necessary investment when you have major changes affecting civilization – which we are now amidst. Case in point, let me offer a few examples.

Over the last 20 years, the first generation of this century, gold outperformed virtually every other asset. If you take the S&P 500 and reinvest your dividends (which can happen automatically if you were to buy an S&P ETF) your initial investment would have been multiplied threefold. That’s good. However if you would have invested that same sum in gold, your initial investment would have multiplied by fivefold over the last 20 years.

Top Performing Investments

Even more relevant is that gold will almost surely continue to outperform, and by a rising amount, over the next 20 years ahead. Steering investors today into a mix of stocks and bonds, while ignoring gold and commodities – is akin to outfitting your high schooler with a manual typewriter instead of a laptop – something that is both comical and absurd.

My analysis goes far beyond the usual view of gold (among most American investors, at least) as mainly a safe haven in times of unusual turmoil. Rather, several interlinked underlying forces have the potential to propel gold upward.

Here I focus on just one of these: a massively significant change in the relative importance to global growth of the developing world vs. the developed, or high-income world. This may sound arcane, but it’s crucial to understanding a dramatic shift in the investment backdrop.

Prior to the 21st century, high-income countries – accounting for only around 15% of global population – racked up faster growth than poorer, developing countries. The big got bigger while the small got smaller. The disparity was so great that the per-capita GDP of the rich was more than 20 times higher than for the rest.

Starting this century, however, and led by China, growth in the developing world began to quicken and eventually to surpass growth in the developed world. The gap in per-capita GDP narrowed to where high-income countries are nine times, not 20 times, wealthier than the world’s have-nots. Better, but still a long way to go.

What does this have to do with gold? Everything.

Emerging Economies And Commodities

Growth in developing economies is qualitatively different from growth in developed ones. Specifically, growth in developing economies requires a lot more commodities per capita. Developed economies, by contrast, are primarily services-driven. In 2019, about 70% of GDP in developed countries came from services compared to 55% for developing economies. A generation earlier, at the start of this century, the percentages were 65% for developed countries, 45% for developing countries.

A good proxy for commodity needs is per-capita energy use. As long as a country is developing and has a relatively small service sector, its growth will require rising energy usage. Readily available data show that 67% is, roughly speaking, the magic cut-off number. Once a country’s service sector reaches 67% of GDP, per-capita need for energy, and commodities overall, starts to decline.

Currently the service sector accounts for 55% of GDP in the developing world. That leaves 12 percentage points more to reach the magic 67% level. It took 20 years for the figure to climb by 10 percentage points, from 45% to 55%. This suggests we likely face at least another 20 years during which per-capita demand for commodities from developing countries, by far the biggest part of the world, will be rising.

Inevitably this will lead to commodity scarcities and rising commodity prices, accelerated by the push to transition to renewables because of climate concerns. Moreover, rising demand for commodities already has reduced reserves for many critical commodities such as copper. The bottom line is that we face at least two decades of pressure on commodities.

It’s currently relevant to take gold and other critical commodities into consideration to include as a part of your investment portfolio. I suggest you decide for yourself whether or not you feel owning gold and various industrial commodities are in alignment with your overall investment objectives.

And I want to emphasize this point… If you talk to an American megalithic financial institution, for example, BlackRock (which manages trillions of dollars) they’ll tell you to allocate your investments. Their recommendation is usually 60% stocks / 40% bonds.

Over the past 20 years…

What were the top performing assets?

Well, here are the facts and the numbers don’t lie.

Since 2000, gold bullion’s performance has outpaced nearly all other major asset classes. That’s measured on total returns including accounting for dividends.

Let’s take a look at the numbers:

- Gold: 530.57%

- Baa Corporate Bond: 321.84%

- S&P 500 (includes dividends): 298.61%

- Real Estate: 200.29%

- US T. Bond: 140.54%

- 3-month T.Bill: 41.18%

Gold Bullion’s Edge Over Bond Markets

Traditional gold storage and ownership offer no investment yield. This is one of the most commonly cited disadvantages of investing in gold compared to more liquid assets. Yet gold bullion bested the top yield-producing assets in the bond markets.

The Baa Corporate Bond has seen consistent growth and has been a good investment. Although, returns since 2000 still fall way behind gold.

The US T. Bond has experienced fluctuations but had a positive performance. The three-month T.Bill, on the other hand, had disappointing performance over a 20 year time frame.

Wrap Up

Gold bullion has surpassed nearly all major high-performing stock markets since 2000. When taking into consideration the performance of the top asset classes over the last 20 years- the old 60 / 40 investing rule is really archaic advice. You’ll hear the same narrative and consensus from Vanguard, Fidelity, and virtually all the major financial institutions. They all push this no-longer-relevant 60 /40 investment diversification as if it were gospel. I have nothing against these financial institutions but if you just look at the history of the past 20 years, which I believe are unique, it might behoove you to question that advice.

What you have witnessed in the investment sphere over the past 20 years is likely to continue onwards but on steroids.

So, take some of their advice but also think for yourself.

What asset class did really well while the world was facing an unprecedented pandemic?

What’s outpaced other asset classes when emerging / developing economies are rapidly growing?

What’s performed well while the globe is hyper focused on a transformation to green renewable energy infrastructure?

Well, what happened is that gold did exceptionally well…

Are there any signs these trends are going to change? Not really.

Are there signs that these trends are going to accelerate? Many.

Therefore, you should consider holding gold (at least as a percentage) of your portfolio. I’m not saying it should be 100%. I’m not saying it should be 5% to 20%. I’m just saying- see gold and commodities as a ballast.

*data compliments of Kinesis Money*

*empirical data compliments of NYU Stern*